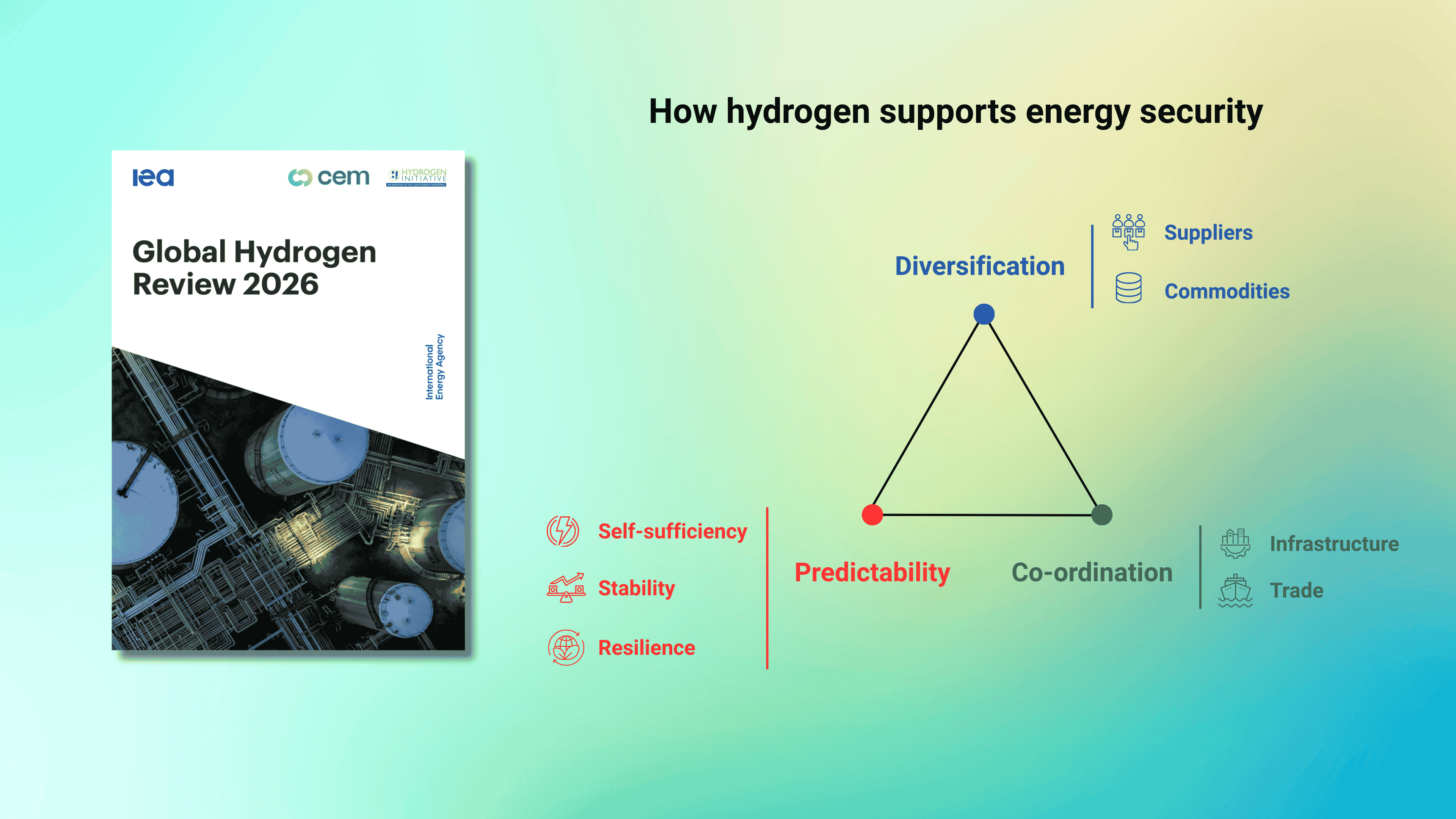

IEA Global Hydrogen Review 2026: green hydrogen can help prevent the next food and energy crisis

The International Energy Agency’s annual Global Hydrogen Review is an essential benchmark for assessing the hydrogen sector’s progress. The sixth edition, launched this week, reads differently from previous years. The usual focus on electrolyser capacity and investment flows gives way to a wider question: what role can hydrogen play in strengthening energy and food security?

The consequences of the Middle East conflict have echoed far beyond the region. Disrupted supply chains, compounded by rising natural gas prices, pushed urea prices to double between January and May 2026. The heaviest impact has fallen on import-dependent agricultural economies in Africa and Asia. Morocco meets 100% of its ammonia demand with imports. Brazil, Australia, South Africa and Thailand import all of their urea, 40-85% of which comes from the Middle East.

The IEA's conclusion is unequivocal:“Renewable hydrogen cannot provide an immediate response in the current crisis, but it can become an important element of strategies to improve long-term energy and food security.”

We fully agree. Green hydrogen may not be able to solve today’s crisis overnight. But it can reduce exposure to the next one by helping countries produce fertilisers, fuels and industrial products from domestic renewable resources, or source them from a wider range of partners, rather than relying on imported fossil fuels.

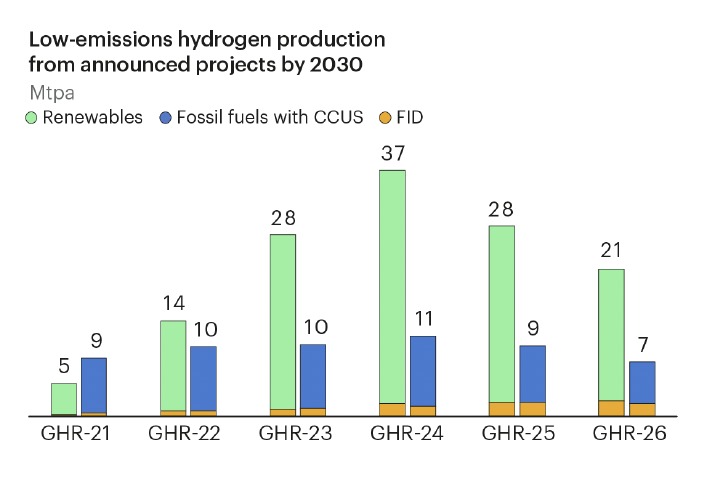

The report confirms that “low-emissions” hydrogen production grew by 20% in 2025 to almost 1 Mt. This year it is expected to break through the 1% threshold of global hydrogen production. Small numbers still, but the direction is right. Made with renewable electricity and water, green hydrogen can have almost no associated emissions. We continue to challenge the IEA to define a cut-off point for what it considers “low-emissions hydrogen” when making hydrogen from fossil fuels with CCUS.

China continues to lead on electrolysers, accounting for nearly three-quarters of new installations in 2025. The IEA notes some deceleration, driven by surplus manufacturing capacity and unsustainable internal competition. But new support schemes announced in the second half of 2025 to expand hydrogen into new sectors and reduce reliance on fossil fuel imports should help reinvigorate the market. In Europe the first large-scale projects are expected to come online in 2026, but slow policy implementation keeps holding back scale-up. The IEA highlights that 22 Mt of potential production could miss any chance of operating by 2030 if investment decisions on announced projects are not taken by early 2027. Two-thirds of that sits in Europe, North America and Latin America.

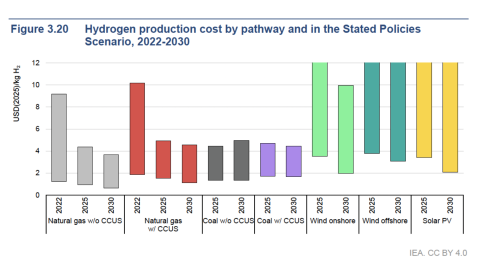

On cost, the IEA’s analysis is useful but needs to be read carefully. The cheapest green hydrogen by 2030 will be in northern China, where optimised combinations of solar and wind can bring production costs below USD 2/kg. Indeed, this is where the world’s largest green hydrogen producing asset is located: GH2 member Envision’s Chifeng project. Some locations in Europe could fall to USD 3.5/kg, while the Middle East, India and Chile could reach just above USD 3/kg.

The IEA suggests blue hydrogen with CCUS could be the most cost-competitive low-emissions option in regions with abundant gas resources, potentially just above USD 1/kg (see the figure below). But this is largely theoretical. No projects are live that achieve anything close to that cost while also meeting 95% carbon capture rates and minimum methane leakage. With economies of scale, green hydrogen remains the most credible path to energy resilience, particularly for regions with strong solar and wind resources.

The Africa chapter is the standout addition to this year's report. The IEA rightly highlights that green hydrogen development on the continent must be tied to wider development goals, not just export projects. Expanding domestic green ammonia production could improve access to nitrogen fertilisers, reduce exposure to price volatility, and support food production. Yet only one out of 31 projects announced for 2030 has reached FID. This is exactly what GH2 and RVO set out to understand in our recent report “From Ambition to Bankability”, which examines why projects in Egypt and Morocco are stalling and what it will take to get them over the line. The crux, as the IEA also makes clear, is demand. Without firm offtake agreements, projects don’t reach FID. Without FID, the sector doesn’t scale.

The same logic applies to shipping. The IEA notes that demand for hydrogen-based fuels will not materialise without policy, regulation and clear reward mechanisms. This is why the IMO’s Net-Zero Framework matters so much. It can help create the investment case for scalable zero and near-zero fuels such as green ammonia and green methanol, and ensure that revenues are recycled back into the transition.

During London Climate Action Week next week, GH2 is co-hosting a closed-door workshop on reward mechanisms for zero and near-zero fuels together with RMI, UCL, the UN Climate Champions and Ambition Loop. The outputs will feed directly into IMO negotiations ahead of key committee meetings later this year.

IMO member states now have a clear set of options if they wish to adopt a framework in line with the IMO’s emissions reduction strategy, captured neatly by Professor Tristan Smith here. GH2 and a coalition of businesses and partner organisations continue to urge Member States to adopt the Net-Zero Framework this year and give the industry the certainty it requires.

We will also participate in the Global Energy Transition and Electrification Summit, co-organised by the UK Department for Energy Security and Net Zero, E3G, We Mean Business Coalition and the Global Renewables Alliance, which GH2 co-founded. It promises to be a busy week. See our full schedule and get in touch if you are around!

Krystyna Serdiuk,

Communications Associate, GH2